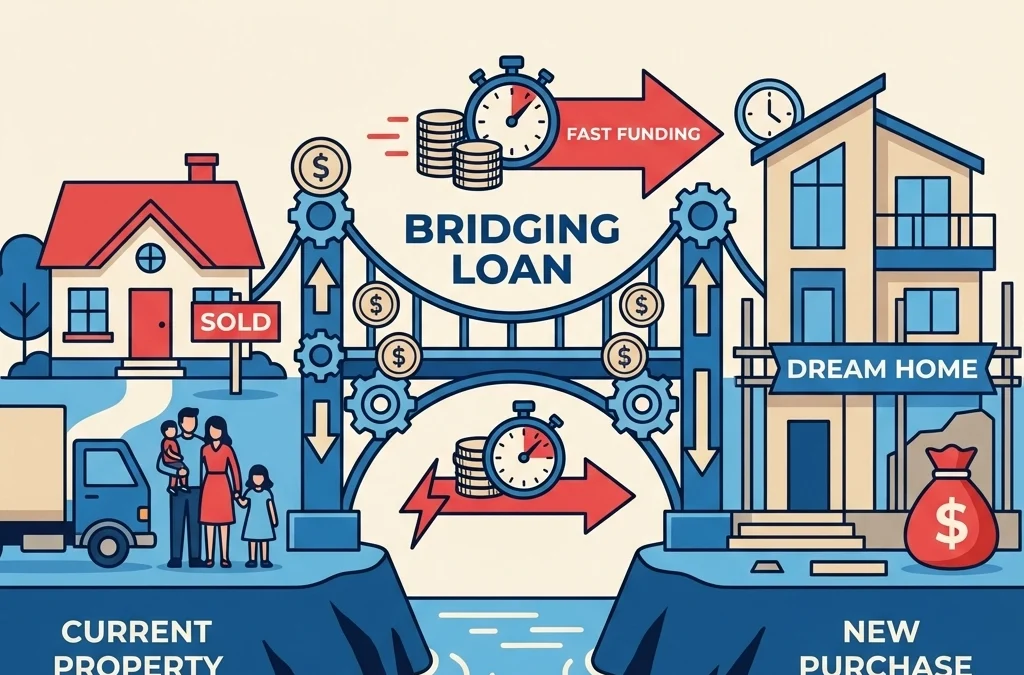

When time is of the essence in property transactions, traditional mortgages often fall short. A bridging loan offers the speed and flexibility that buyers need when conventional financing simply can't keep pace with market demands or personal circumstances.

What Are Bridging Loans?

A bridging loan is a short-term financing solution designed to bridge the gap between buying a new property and selling an existing one. Unlike traditional mortgages that can take 6-8 weeks to complete, bridging loans can provide funds within days, making them invaluable for time-sensitive property purchases.

These loans work by using your existing property as security while you purchase your next home. The lender places a charge against your current property, giving you immediate access to funds for your new purchase. Once your existing property sells, the proceeds pay off the bridging loan.

How Bridging Loans Work in Practice

The process starts with a rapid application and valuation. Lenders assess both your existing property's value and the property you're purchasing. Most bridging loan providers can offer loan-to-value ratios of up to 75% of your current property's worth, though some specialist lenders may go higher depending on circumstances.

Unlike traditional mortgages, bridging loans typically operate on an interest-only basis during the loan term. This means monthly payments remain manageable while you're managing two properties. The capital amount is then repaid in full when your original property completes its sale.

How Fast Can I Get a Bridging Loan?

Speed is the primary advantage of bridging finance. Where traditional mortgages require extensive documentation, credit checks, and lengthy approval processes, bridging loans can complete in as little as 7-14 days from application to funds being available.

For urgent transactions, some specialist lenders can even provide decisions within 24-48 hours and release funds within a week. This speed comes from streamlined underwriting processes that focus primarily on property values rather than extensive income verification.

The fastest completions typically occur when:

- Property valuations can be conducted quickly

- Legal work on both properties progresses smoothly

- All documentation is provided upfront

- The borrower has strong equity in their existing property

In one recent case, Hunter Capital helped a client secure bridging finance in just 5 working days to prevent losing their dream home when their buyer encountered last-minute delays.

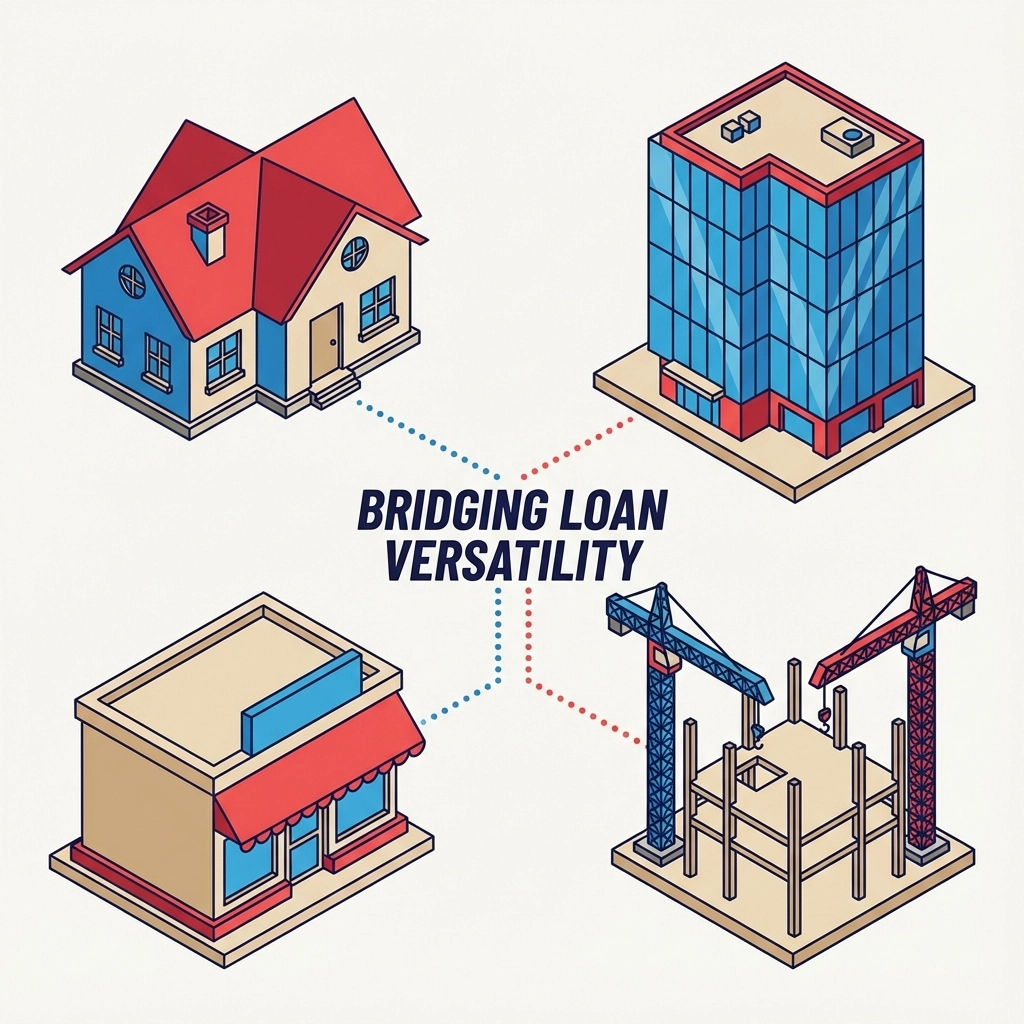

What Properties Can Bridging Loans Be Used For?

Bridging loans demonstrate remarkable versatility in property types and purposes. Residential properties form the most common use case, whether for family homes, investment properties, or holiday homes.

Commercial properties also qualify for bridging finance, including office buildings, retail spaces, industrial units, and mixed-use developments. Property developers frequently use bridging loans for land purchases and development projects where traditional commercial mortgages prove too slow or inflexible.

Investment properties represent another major category, particularly for landlords building portfolios or investors purchasing properties for renovation and resale. The speed of bridging finance allows investors to secure properties at auction or take advantage of time-sensitive opportunities that require immediate funding.

Unique property types that traditional lenders often reject also become accessible through bridging finance. These include non-standard construction properties, buildings requiring significant renovation, or properties with unusual tenancy arrangements.

However, certain limitations apply. Lenders typically avoid properties with structural issues, contaminated land, or properties involved in legal disputes. The key criterion remains whether the property provides adequate security for the loan amount.

Understanding Bridging Loan Costs

Bridging loans carry higher costs than traditional mortgages, reflecting their short-term nature and rapid deployment. Monthly interest rates typically range from 0.5% to 1.5% per month, equivalent to annual rates of 6% to 18%.

Several factors influence pricing:

- Loan-to-value ratio – lower LTV ratios attract better rates

- Property type – standard residential properties receive preferential pricing

- Borrower experience – experienced property investors often secure better terms

- Exit strategy – clear sale timelines can improve rate offerings

Additional costs include arrangement fees (typically 1-2% of the loan amount), valuation fees, legal costs, and broker fees. When calculating total costs, factor in these additional expenses alongside monthly interest payments.

Despite higher costs, bridging loans often prove cost-effective when they enable profitable transactions or prevent losses from failed property chains.

What Are the Risks of Bridging Finance?

Bridging loans carry specific risks that require careful consideration. The primary risk involves exit strategy failure – if your existing property doesn't sell as planned, you're left servicing expensive bridging loan interest while potentially facing extended marketing periods.

Interest rate risk poses another concern. With monthly interest rates significantly higher than traditional mortgages, extended loan periods can become prohibitively expensive. A property that takes 12 months to sell instead of the anticipated 6 months effectively doubles your interest costs.

Market risk affects both your existing property sale and new purchase. Falling property values could create negative equity situations, particularly problematic with bridging loans' higher loan-to-value ratios.

Liquidity risk emerges if personal circumstances change during the loan term. Job loss, illness, or other financial pressures can make monthly interest payments difficult to maintain.

To mitigate these risks:

- Ensure realistic property sale timelines with estate agent input

- Maintain cash reserves for extended marketing periods

- Consider backup sale strategies, including rental potential

- Only use bridging loans when confident of exit strategy success

Types of Bridging Loans

First charge bridging loans apply when your existing property has no outstanding mortgage. The bridging loan takes primary position, offering lower interest rates due to reduced lender risk. These loans typically provide access to higher loan-to-value ratios and more competitive terms.

Second charge bridging loans work alongside existing mortgages on your current property. The bridging lender takes secondary position, resulting in higher interest rates to compensate for increased risk. However, these loans enable property purchases even when significant mortgage balances remain outstanding.

Regulated bridging loans fall under Financial Conduct Authority oversight when the property serves as your main residence. These loans include additional consumer protections but may involve longer application processes.

Unregulated bridging loans apply to investment properties and second homes, offering greater flexibility in terms and faster processing times.

When Bridging Loans Make Sense

Bridging loans excel in specific scenarios where traditional finance falls short. Property chains benefit significantly, particularly when your buyer encounters delays but your new purchase cannot wait.

Investment opportunities often require immediate action. Property auctions demand completion within 28 days, making bridging loans essential for successful bidding. Similarly, below-market-value properties or distressed sales require quick decisions that traditional mortgages cannot accommodate.

Renovation projects frequently need bridging finance, especially when properties require significant work before meeting traditional mortgage lending criteria. Developers and property renovators rely on bridging loans to purchase, improve, and refinance or sell properties.

Competitive markets where sellers favor cash buyers can be accessed through bridging loans, providing the equivalent of cash purchase speed while using property equity as funding.

Getting Started with Bridging Finance

Successful bridging loan applications require preparation and expert guidance. Start by obtaining a realistic valuation of your existing property and clear timelines for its sale. Estate agents can provide crucial market insights that support your exit strategy.

Calculate total costs carefully, including interest payments for various time scenarios. Consider what happens if your property takes longer to sell than anticipated, and ensure you can service the loan during extended periods.

Professional advice proves invaluable given bridging loans' complexity and cost. Experienced brokers can access specialist lenders, negotiate better terms, and structure deals that optimize your specific circumstances.

At Hunter Capital, we specialize in fast-track bridging finance solutions tailored to individual client needs. Our extensive lender panel includes specialist bridging loan providers offering competitive rates and flexible terms. Whether you're facing property chain delays, pursuing investment opportunities, or need funds for development projects, our team can structure appropriate bridging solutions.

Contact Hunter Capital today to discuss your bridging loan requirements. Our experienced advisers provide same-day initial consultations and can typically provide loan decisions within 48 hours. Don't let timing constraints prevent you from securing your next property – bridging finance could be the solution you need.

Facebook Summary: Bridging loans provide fast property funding when traditional mortgages are too slow, completing in just 7-14 days. Perfect for breaking property chains, investment opportunities, and time-sensitive purchases, though costs are higher than standard mortgages.