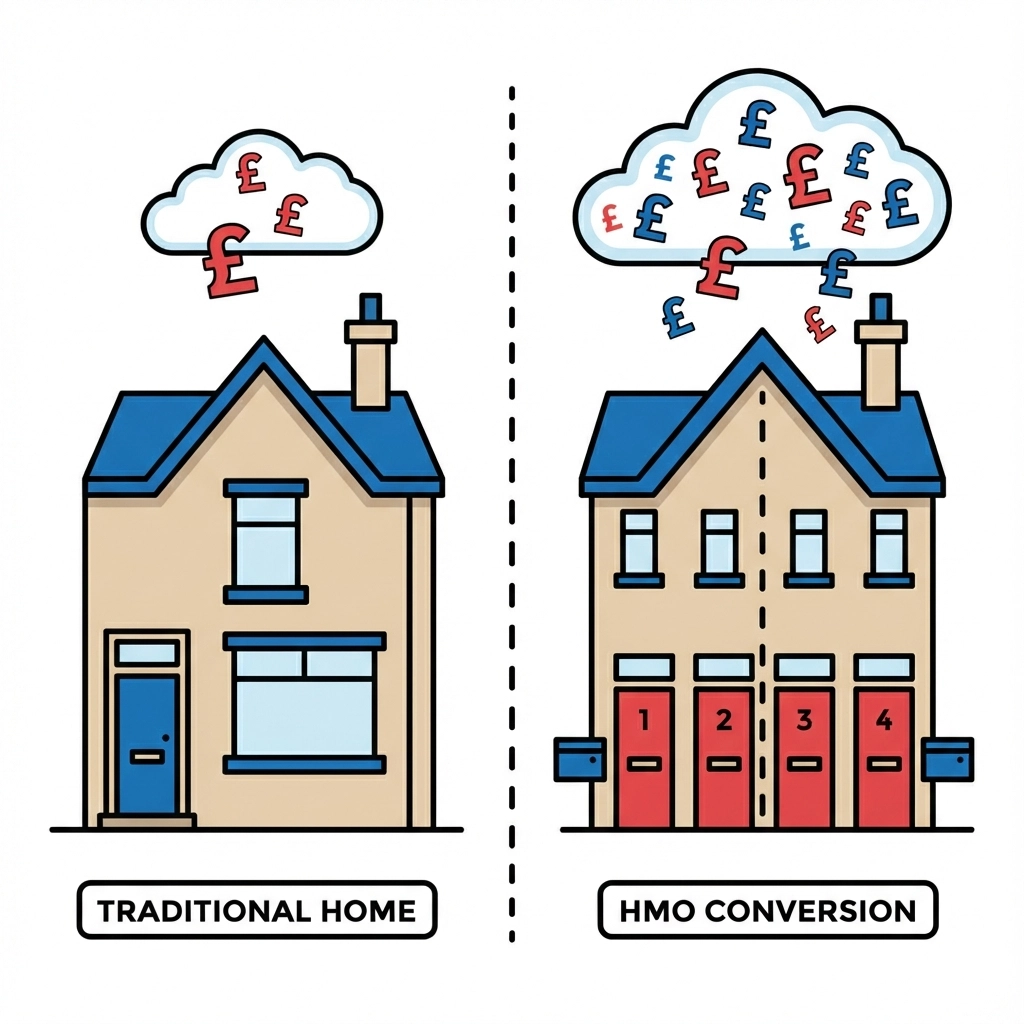

House in Multiple Occupation (HMO) properties are quietly becoming the smart money's favourite investment strategy. While standard buy-to-let landlords struggle with yields averaging 7.4% across the UK, experienced HMO investors consistently achieve returns that leave traditional property investment in the dust.

The difference isn't marginal: it's transformational. Where a standard buy-to-let might generate £400 monthly profit, a comparable HMO can deliver £1,000-£1,500. That's not just better returns; it's a completely different investment category.

Why HMO Yields Demolish Standard Buy-to-Let Returns

The mathematics of HMO investment fundamentally differs from standard buy-to-let properties. Instead of one household paying one rent, HMO landlords collect individual rent from three or more separate tenants sharing the same property.

This creates multiple income streams from a single asset. A four-bedroom HMO in Manchester might collect £450 per room monthly: that's £1,800 total rent versus perhaps £900 for the same property let to a family. The gross yield difference becomes immediately apparent.

Recent market data reveals striking regional variations in standard buy-to-let yields. The North East leads at 9.2%, followed by the North West at 8.4%. Greater London lags at 6%, with the South East achieving 6.5%. HMO properties in these same regions consistently outperform these figures by significant margins.

The rental arbitrage becomes even more compelling when considering void periods. Traditional buy-to-let properties lose 100% of their income when tenants leave. HMO landlords continue collecting rent from remaining tenants while finding replacements for individual rooms.

The Numbers Game: HMO vs Standard Buy-to-Let

Professional HMO investors report achieving double to quadruple their return on investment compared to standard buy-to-let colleagues. This performance gap stems from several mathematical advantages.

Income multiplication effect: A typical three-bedroom house in Birmingham might rent for £750 monthly as a standard let. Convert it to a four-bedroom HMO, and individual room rents of £400-450 generate £1,600-1,800 monthly: more than doubling income from the same asset.

Reduced void impact: When a standard buy-to-let tenant leaves, landlords face complete income loss during void periods. HMO landlords typically maintain 75% occupancy even during tenant transitions, dramatically improving cash flow consistency.

Capital efficiency: HMO investors often recycle capital more effectively. After purchasing and converting a property, the improved rental yield allows faster mortgage paydown and earlier equity release for additional investments.

One experienced investor recently shared their portfolio comparison: their standard buy-to-let properties average £300 monthly profit, while comparable HMO conversions generate £1,200 monthly. That's four times the return from similar capital deployment.

Getting Started: The HMO Mortgage Landscape

Securing HMO financing requires navigating a more complex lending landscape than standard buy-to-let mortgages. Fewer lenders offer HMO products, and those that do impose stricter criteria.

Specialist lender requirements: Mainstream banks rarely offer HMO mortgages. Specialist lenders typically require larger deposits: often 25-30% versus 20-25% for buy-to-let properties. Interest rates also run higher, typically 0.5-1% above equivalent buy-to-let products.

Experience prerequisites: Many HMO lenders require demonstrated landlord experience. First-time investors often need to start with standard buy-to-let properties before accessing HMO financing options.

Property standards: HMO mortgages require properties meeting specific safety and space requirements. Bedrooms must typically measure at least 6.5 square metres, with adequate bathroom and kitchen facilities for the number of tenants.

The application process involves additional complexity. Lenders assess rental projections based on individual room rates rather than whole-property lettings. They scrutinise local rental markets more thoroughly and often require detailed conversion plans.

Navigating HMO Challenges

Higher returns accompany increased responsibilities and risks. Successful HMO investors understand these challenges and plan accordingly.

Management intensity: HMO properties require significantly more hands-on management than standard buy-to-lets. Landlords handle multiple tenancy agreements, coordinate shared space maintenance, and manage more frequent tenant turnover. Individual tenants typically stay 6-12 months versus 1-2 years for family lets.

Regulatory compliance: HMO properties face stricter regulations than standard lets. Properties housing five or more tenants require mandatory HMO licensing. Even smaller HMOs often require additional licensing in certain council areas. Fire safety requirements, electrical testing, and gas safety checks occur more frequently.

Higher conversion costs: Transforming standard properties into compliant HMOs requires significant upfront investment. Bathroom additions, bedroom conversions, fire safety installations, and kitchen expansions typically cost £10,000-25,000 per property.

Tenant screening complexity: Managing multiple tenants requires more sophisticated screening processes. Landlords must consider tenant compatibility, payment reliability, and lifestyle factors that affect shared living situations.

Most successful HMO investors employ professional management companies to handle day-to-day operations. This reduces personal time investment but impacts net yields by 8-12% management fees.

Securing HMO Financing: The Specialist Route

Working with experienced mortgage brokers becomes essential when pursuing HMO financing. The specialist nature of these products means direct lender approaches often prove unsuccessful.

Broker advantages: Specialist brokers maintain relationships with HMO lenders and understand specific product criteria. They can pre-qualify applications and identify suitable lenders before formal submissions, saving time and protecting credit scores.

Portfolio lending: Experienced HMO investors often utilise portfolio lending approaches. Rather than individual property mortgages, portfolio lenders assess entire property portfolios, often providing better rates and terms for substantial investments.

Refinancing strategies: Many HMO investors use initial bridging finance for property purchase and conversion, then refinance onto long-term HMO mortgages once properties achieve full rental income. This approach maximises leverage while maintaining cash flow.

The lending landscape continues evolving as HMO investment gains mainstream acceptance. More lenders now offer competitive HMO products, though specialist knowledge remains crucial for accessing optimal terms.

Making HMO Investment Work

Successful HMO investment requires careful property selection and market analysis. Not all areas suit HMO strategies, and local council attitudes toward HMOs vary significantly.

Location criteria: University towns, major employment centres, and areas with young professional populations typically offer strongest HMO rental demand. Properties near transport links and local amenities command premium room rates.

Due diligence: Investigating local planning policies, HMO licensing requirements, and Article 4 Direction areas prevents costly surprises. Some councils actively discourage HMO conversions in certain neighbourhoods.

Financial modelling: Accurate financial projections require understanding local room rates, void periods, management costs, and conversion expenses. Conservative estimates prevent over-leveraging and cash flow problems.

Professional team: Successful HMO investors build relationships with experienced solicitors, accountants, contractors, and managing agents who understand HMO-specific requirements.

The learning curve for HMO investment exceeds standard buy-to-let property, but the financial rewards justify the additional effort for committed investors.

Next Steps for HMO Investment

HMO mortgages represent a sophisticated investment strategy delivering superior returns for experienced property investors. While the entry barriers exceed standard buy-to-let investment, the income potential makes HMO properties increasingly attractive in today's challenging yield environment.

Getting started requires careful planning, adequate capital, and professional guidance. The complexity of HMO financing means working with specialists who understand both the lending landscape and regulatory requirements.

For investors ready to move beyond basic buy-to-let strategies, HMO properties offer a proven route to enhanced rental yields and improved portfolio performance. The key lies in thorough preparation and realistic expectations about the additional work involved.

Ready to explore HMO mortgage options for your next investment? Contact our specialist team to discuss how HMO financing could enhance your property portfolio returns and access the higher-yield opportunities that traditional buy-to-let investing simply cannot match.