Facebook Summary: If you’re in Oldham and your mortgage has slipped onto the lender’s SVR, it can feel like you’re just throwing money away every month. With bills going up everywhere (even the price of a brew), a quick February mortgage health check could help you cut your payments before March.

Let's be honest, most of us in Oldham don’t think about our mortgage until something forces us to. The monthly payment goes out, you get on with life, and you hope it’s fine. But if you’re sitting on your lender’s Standard Variable Rate (SVR), it can honestly feel like you’re just throwing money away — especially when everything else is creeping up too (food, fuel, and even the cost of a quick brew).

Think of this as your mortgage MOT. You wouldn’t drive up and down the A627(M) for years without checking the car’s running properly, right? Your mortgage deserves the same attention — because for most people it’s the biggest bill going out each month.

What Exactly Is a Mortgage Health Check?

A mortgage health check is simply taking stock of where you stand. It means looking at:

- What rate you're currently paying

- How long you've been on that rate

- What deals are available now

- Whether remortgaging could save you money

- If your current mortgage still fits your life

It's not complicated, and it doesn't require a finance degree. You just need to know what you're paying and whether you could do better. Spoiler: you almost certainly can if you're on an SVR.

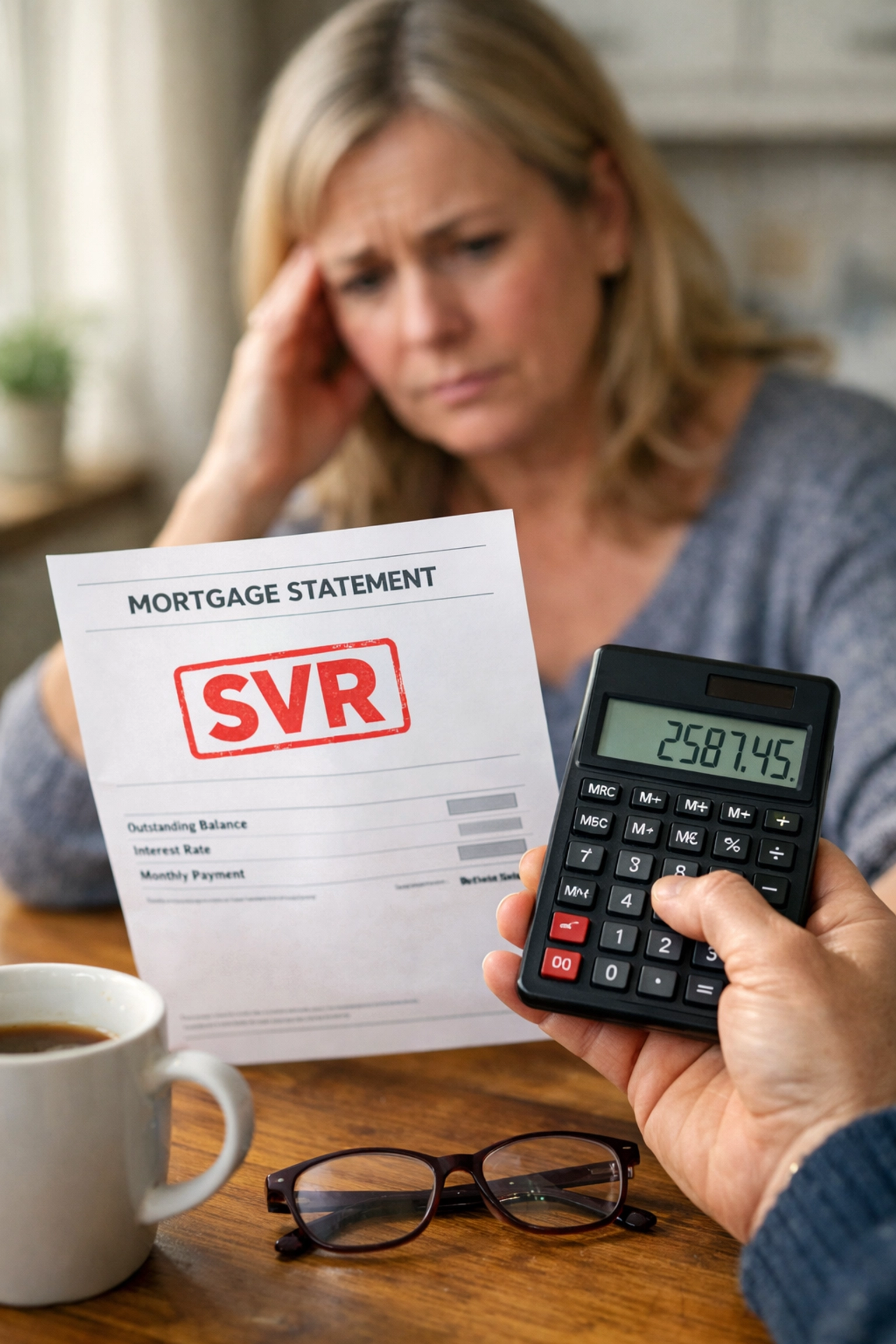

The SVR Trap: Why It Feels Like You're Throwing Money Away

Here’s how it usually happens (and it’s so common). You took a mortgage a few years back, fixed it for two or five years, and everything was fine. Then the deal ends… and without making a big song and dance about it, the lender moves you onto their SVR. A letter lands, you skim it between work and life admin, and that’s it — you’re paying more each month without really choosing to.

SVR is basically the lender’s “default” rate once your initial deal ends. It’s nearly always higher than the better fixed rates on the market. And that extra cost doesn’t feel “real” until you look at what it could be doing instead.

On a £200,000 mortgage, even a 2% gap can be around £200–£300 extra per month. In real-life terms, that’s money that could be:

- a few decent shops at Tesco in Oldham

- keeping the heating on without stressing

- covering the car costs, kids’ stuff, or just giving you breathing space

Instead, it’s just disappearing into the mortgage — month after month. That’s why SVR feels like throwing money away.

Why do lenders do this? Because they can. They rely on people being busy and not wanting the hassle of switching. If you’ve been hit with rising costs everywhere else, this is one place you might be able to claw some money back.

Why February Matters

February might seem like a random month for a mortgage review, but there's method to the madness. Here's why this timing works:

Product launches ahead of the new tax year: Lenders often refresh their mortgage products in spring, particularly around March and April. Getting in now means you can lock in current rates before any potential changes.

Avoiding the spring rush: By April and May, the property market typically picks up steam. Mortgage brokers get busier, applications take longer to process, and you're competing for lender attention. February is quieter, you'll get faster service.

Quarter-end pressures: Many lenders have targets to hit by the end of Q1 (March 31st). This can mean competitive rates and more flexibility in February as they push to meet those numbers.

Time to complete before rates shift: Even if you apply today, remortgaging takes 4-8 weeks on average. Starting in February means you're sorted well before summer, when the Bank of England typically reviews interest rates.

How to Tell If You're on the Wrong Rate

Not sure where you stand? Here's a quick reality check:

Check your mortgage statement: Your current rate should be listed. If it's above 5.5% right now, you're almost definitely paying too much.

Look at your paperwork: Can you find your original mortgage offer? Check when your fixed or tracker period ended. If it was more than a few months ago, you're on the SVR.

Do the maths: Use an online mortgage calculator. Put in your remaining balance and the current average fixed rates (around 4-5% depending on your LTV). Compare what you'd pay versus what you're paying now. Eye-opening, isn't it?

Call your lender: Ask them directly: "What rate am I on, and is it your SVR?" They have to tell you. If the answer is yes, it's time to move.

Practical Steps to Lock in a Better Rate Before March

Right, you've confirmed you're overpaying. What now? Here's your action plan:

1. Work out your numbers

- Current mortgage balance

- Property value (estimate is fine, check Rightmove for similar homes in your area)

- Your loan-to-value ratio (LTV): that's your mortgage divided by your property value

- Monthly budget for payments

2. Check your credit score

Get your free credit report from Experian, Equifax, or TransUnion. A better score means access to better rates. If there are errors, get them fixed now, it matters.

3. Calculate early repayment charges (ERCs)

Still technically in a fixed period? Check if there's a penalty for leaving early. Sometimes it's worth paying if the savings are significant, but you need to do the maths.

4. Research current rates

Look at comparison sites, but remember they don't show everything. Mortgage brokers have access to exclusive deals you won't find online.

5. Speak to a broker

This is genuinely the smart move. A good broker knows the market inside out, can access better rates, and handles the paperwork. For Oldham homeowners, working with a local broker who understands the area's property market makes a real difference.

The Oldham Advantage (And Why It Matters Right Now)

If you’re a homeowner in Oldham, you’re often in a decent spot for remortgaging. Prices here are still more sensible than central Manchester, and that can help your loan-to-value (LTV) look healthier — which can open up better mortgage rates.

Whether you’re in Royton, Chadderton, Shaw, Lees, Saddleworth, or near the town centre (around Tommyfield Market / the Spindles area), there’s a good chance your equity has improved over the last few years. And the better your LTV, the more choice you usually get.

Also, doing this with a local mortgage broker helps because we actually know the area. If you tell us you’re near Alexandra Park or you’re looking at a typical Oldham terrace vs a newer build, we get it — and we’ll guide you to lenders that are comfortable with your property type and situation.

What About Remortgaging Costs?

Let's address the elephant in the room. Yes, remortgaging comes with some costs:

- Valuation fee (sometimes free, usually £250-500)

- Legal fees (often free through cashback offers)

- Arrangement fee (typically £0-1,500, sometimes added to the mortgage)

- Broker fee (many brokers don't charge you directly)

Sounds like a lot? Compare it to what you'll save. If you're dropping your rate by even 1%, you'll likely recoup those costs within a few months and save thousands over the mortgage term. It's basic maths, and the numbers almost always work in your favour.

Common Mistakes to Avoid

Don't just stick with your current lender: Sure, it's easier, but you'll probably get a better deal by switching. Loyalty doesn't pay in the mortgage world.

Don't wait until your deal expires: Start looking 3-6 months before. You can lock in rates months in advance.

Don't assume you can't remortgage: Self-employed? Bad credit in your past? There are lenders who specialise in these situations. Don't rule yourself out without checking.

Don't forget to factor in fees: The lowest rate isn't always the cheapest deal overall. Look at the total cost.

Frequently Asked Questions

How long does remortgaging take?

Typically 4-8 weeks from application to completion, though it can be quicker if everything's straightforward.

Will my credit score be affected?

Applications create a hard search on your credit file, but one or two searches for mortgage purposes won't significantly harm your score. Multiple applications in a short time can be a red flag though.

Can I remortgage if I'm self-employed?

Absolutely. You'll typically need 2-3 years of accounts or SA302 forms, but plenty of lenders work with self-employed borrowers.

What if my property value has dropped?

You might have a higher LTV than before, which could limit your options, but you'll still likely find better rates than your SVR.

Is now a good time with rates where they are?

Rates are significantly better than they were 12-18 months ago. While we can't predict the future, waiting for the "perfect" time often means missing out on real savings today.

Do I need to get my home revalued?

Your lender will arrange this as part of the remortgage process. You don't typically need to do anything yourself.

Don't Let March Pass You By

Look, here’s the bottom line: with the cost of living the way it is, nobody in Oldham wants to feel like they’re wasting money. If you’re on an SVR, that’s often exactly what’s happening — more money leaving your account each month for the same home, simply because the old deal ended.

February is a good time to sort it. Things are generally calmer, there are still competitive products around, and you’ve got time to get it done before the spring rush.

If you take one thing from this post, let it be this: being on SVR can feel “normal” because you get used to the payment — but it can also be one of the easiest places to stop throwing money away. Your Oldham home should be helping you feel secure, not draining you month after month. Let’s fix that.

Ready to Lock in a Better Rate?

We help Oldham homeowners navigate the mortgage market every single day. Whether you're stuck on an SVR, coming to the end of a fixed term, or just wondering if you could do better, we'll give you straight answers and access to deals you won't find on comparison sites.

Book your free mortgage consultation with Hunter Capital today. No jargon, no pressure: just honest advice on whether remortgaging makes sense for you. Let's make sure your biggest monthly payment is actually working in your favour.