Oldham is a fantastic place to call home. Whether you’re eyeing up a terrace in Chadderton, a family semi in Royton, or something with a bit of character near Saddleworth, the local property market is buzzing. But let’s be honest: finding the right mortgage can feel a bit like trying to navigate the M60 at rush hour, confusing, stressful, and full of unexpected turns.

At Hunter Capital, we see people making the same mistakes time and time again. These errors don't just cause stress; they can cost you thousands of pounds over the life of your loan.

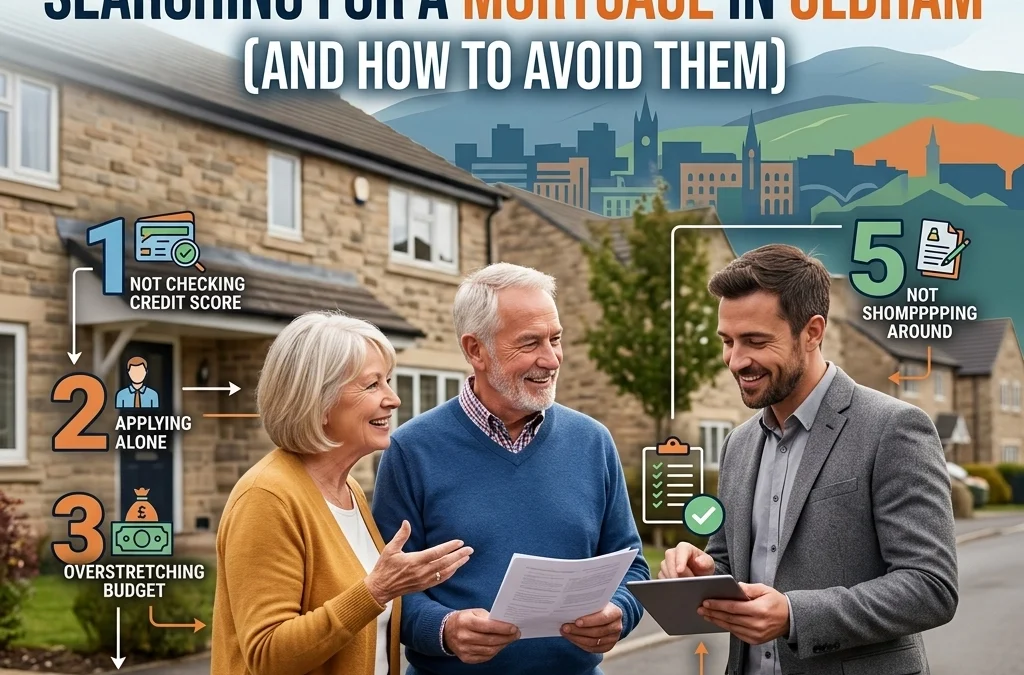

If you’re looking to get on the ladder or move house in the OL postcode area, here are the seven most common mistakes we see, and more importantly, how you can avoid them.

1. Not Checking Your Credit Score Early Enough

Many people wait until they’ve found their dream home near Tommyfield Market before they even look at their credit file. This is a huge risk. Your credit score is the first thing a lender looks at to decide if you’re "mortgage-worthy" and what interest rate they’ll offer you.

A single missed mobile phone payment from three years ago or an old address still linked to a bank account can derail your application.

How to avoid it:

- Check your report through services like Experian, Equifax, or TransUnion at least six months before you plan to buy.

- Ensure you are on the electoral roll at your current Oldham address.

- Pay down any small outstanding debts and avoid opening new credit lines (like "buy now, pay later" schemes) in the months leading up to your application.

2. Only Visiting Your Local High Street Bank

It’s a common habit. You’ve banked with the same big name in Oldham town centre for twenty years, so you assume they’ll give you the best deal. While loyalty is great, in the mortgage world, it rarely pays off.

Your bank only has access to their own products. They won’t tell you if a smaller lender or a specialist firm has a rate that’s 0.5% lower, which could save you a fortune.

How to avoid it:

- Look at the "whole of market." There are dozens of lenders out there, some you’ve never heard of, that might have criteria better suited to your specific situation, especially if you are self-employed or have a complex income.

- Check our our lenders page to see the variety of options available beyond the big banks.

3. Forgetting the "Hidden" Costs of Moving

In Oldham, property prices can be more affordable than in central Manchester, but the associated costs of buying remain the same. Many buyers save up just enough for a 5% or 10% deposit and then realise they can't afford the rest.

If you don't budget for the extras, you might find yourself in a tight spot just as you're about to exchange contracts.

How to avoid it:

Budget for the following "hidden" extras:

- Stamp Duty Land Tax: Depending on the price and whether you’re a first-time buyer.

- Surveyor Fees: Essential for checking the condition of that lovely Victorian terrace in Lees.

- Solicitor/Conveyancing Fees: The legal work to transfer the property.

- Product Fees: Some of the best mortgage rates come with an upfront fee (often around £999).

- Removal Van: Even a local move within Shaw or Failsworth costs money!

4. Not Getting an "Agreement in Principle" (AIP) First

The Oldham property market moves fast. If a well-priced house goes up for sale in a popular spot like Grasscroft, it won’t stay on the market long. If you turn up for a viewing without an Agreement in Principle, the seller might not even take your offer seriously.

An AIP is a document from a lender stating how much they are likely to lend you. It proves you are a "qualified" buyer.

How to avoid it:

- Before you start scrolling through Rightmove, speak to a broker.

- Getting an AIP is usually a quick process and doesn't commit you to a specific house, but it gives you the confidence to bid when you find "the one."

5. Changing Jobs or Increasing Debt Mid-Application

This is a heartbreaker. We’ve seen people get their mortgage approved, only to go out and buy a new car on finance or quit their job for a "better" one before the house sale completes.

Lenders often do a final credit check and employment verification just before they release the funds. If your circumstances have changed significantly, they can, and will, withdraw the mortgage offer.

How to avoid it:

- Keep your finances "boring" until you have the keys in your hand.

- Avoid major career changes (even if it’s a pay rise, the new probationary period can cause issues).

- Don't take out any new loans, credit cards, or car finance until the move is finished.

6. Misunderstanding Fixed vs. Variable Rates

In a fluctuating economy, choosing the wrong type of mortgage can lead to "payment shock." We often meet people who chose a variable rate because it was the cheapest on day one, only to see their monthly payments skyrocket a year later when interest rates rose.

On the flip side, some people lock into a 10-year fixed rate and then realise they want to move house in three years, only to be hit with massive Early Repayment Charges.

How to avoid it:

- Think about your long-term plans. Are you planning to stay in this Oldham home for the long haul, or is it a starter home?

- Read up on latest updates regarding market trends.

- Ask your broker to run the numbers on different scenarios so you know exactly what you’re signing up for.

7. Trying to Do It All Alone

With so many comparison sites online, it’s tempting to try and DIY your mortgage. But those sites don't know the local Oldham market, they don't know which lenders are currently slow with valuations, and they certainly won't fight your corner if the application gets stuck.

A local mortgage broker does more than just find a rate; they manage the entire process from application to completion.

How to avoid it:

- Use a professional who understands the local area and the specific challenges of the current market.

- Whether you need help with buy-to-let or a standard residential move, professional advice is invaluable.

Frequently Asked Questions (FAQ)

Can I get a mortgage in Oldham if I have bad credit?

Yes, it is possible. While the big high street banks might say no, there are specialist lenders who focus on "adverse credit." It often requires a slightly larger deposit, but it’s certainly not an impossible dream.

How much deposit do I really need?

Generally, you need at least 5%. However, having a 10% or 15% deposit will unlock much better interest rates, which could save you a lot of money every month.

What is the difference between a broker and a lender?

A lender (like a bank) provides the money. A broker (like Hunter Capital) acts as the middleman to find the best lender and deal for your specific needs, handling the paperwork and jargon for you.

How long does the mortgage process take in Oldham?

Typically, you should allow 8 to 12 weeks from finding a house to moving in. However, the mortgage offer itself can often be secured within 2 to 4 weeks if your paperwork is in order.

Ready to Find Your Perfect Oldham Home?

Searching for a mortgage shouldn't feel like a chore. At Hunter Capital, we’re proud to be a part of the Oldham community, helping locals navigate the complexities of property finance with ease and transparency.

Whether you're a first-time buyer, looking to refinance, or interested in commercial mortgages, Naz and the team are here to help. We strip away the jargon and focus on getting you the best deal possible.

Don't leave your home ownership dreams to chance.

Book your FREE mortgage consultation with Hunter Capital today!

Facebook Summary:

Buying a home in Oldham? Don't let common mortgage mistakes cost you thousands! Check out our latest guide on the 7 traps to avoid and how to secure the best deal for your next move. 🏠✨