Property insurance in 2026 has become more complex than ever. With rising construction costs, evolving risk landscapes, and stricter lender requirements, understanding the right coverage for your property type isn't just important, it's essential for protecting your investment.

Whether you're a homeowner looking to safeguard your primary residence or a landlord managing rental properties, the insurance landscape has shifted significantly. The difference between adequate coverage and a financial disaster often comes down to understanding exactly what protection you need and where gaps might exist.

The Critical Difference: Homeowner's vs Landlord Insurance

The moment a tenant moves into your property, your insurance needs change entirely. Standard homeowner's insurance policies typically exclude coverage for rental activities, leaving landlords exposed to significant liability risks. A tenant's guest injury, property damage from renters, or business-related claims could result in personal financial responsibility without proper landlord coverage.

Landlord insurance addresses the unique risks of rental properties. Unlike homeowner's policies that assume owner-occupancy, landlord insurance recognizes that tenants introduce different liability scenarios, property usage patterns, and potential damage sources.

What Landlord Insurance Actually Covers

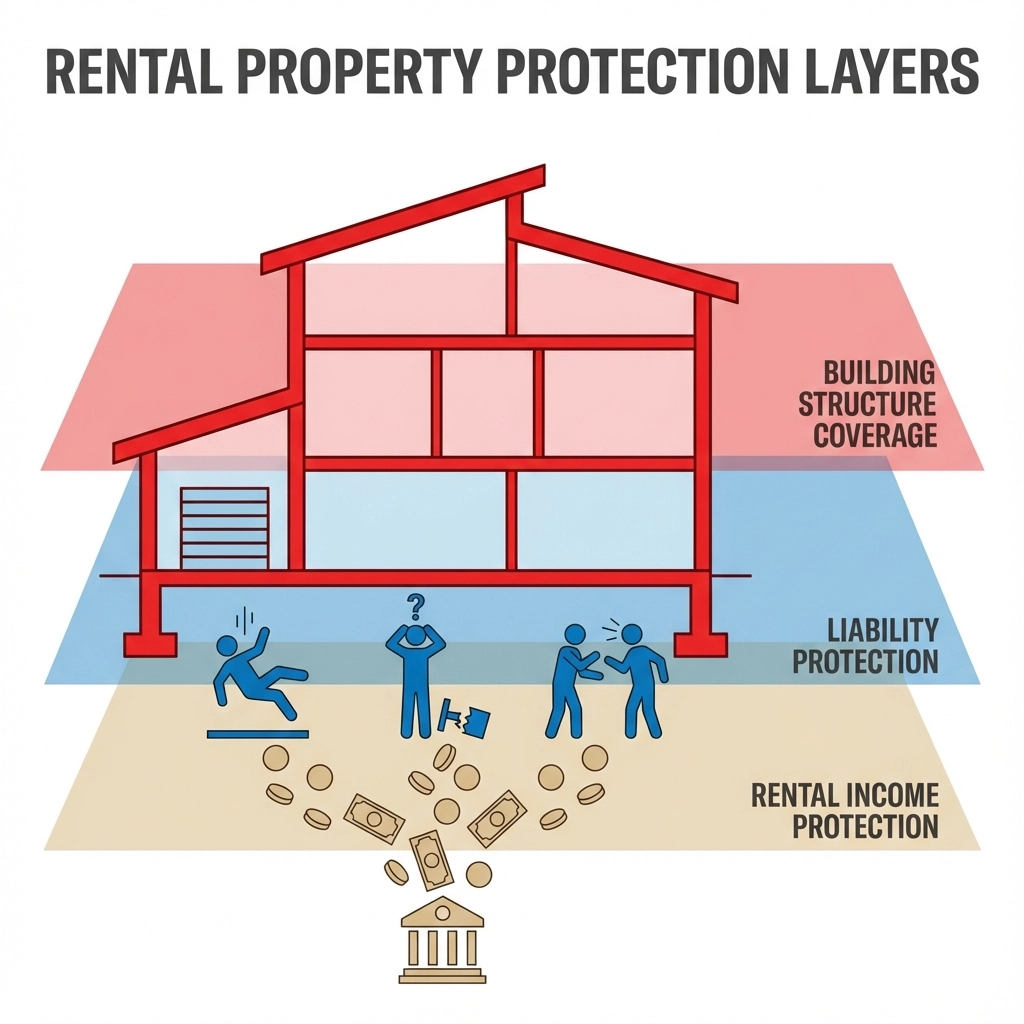

Landlord insurance provides three essential protection layers that standard homeowner's policies don't address:

Property Protection: Coverage extends to the building structure and landlord-owned items like appliances, protecting against fire, wind damage, vandalism, and burglary. This includes detached structures such as garages and storage sheds that tenants might access.

Liability Coverage: Protection when tenants or their guests suffer injuries on the property. With the recommended minimum rising to £1 million for even single-family rentals in 2026, this coverage has become non-negotiable for serious landlords.

Loss of Rental Income: Perhaps the most overlooked yet critical component, this coverage compensates for lost rental income when properties become uninhabitable due to covered events. Given extended construction timelines in 2026, experts recommend coverage spanning 12 to 24 months of rental income.

Essential Coverage Pillars for 2026

Dwelling Coverage Standards

The DP-3 policy remains the gold standard for rental properties, offering "open perils" protection that covers everything except specifically excluded events. The critical 2026 decision involves choosing between Replacement Cost and Actual Cash Value coverage.

With construction material costs remaining elevated, Actual Cash Value policies could leave landlords facing significant shortfalls. Replacement Cost coverage ensures full rebuilding capacity without depreciation deductions, though it comes with higher premiums.

Updated Liability Requirements

Liability coverage recommendations have increased substantially for 2026. Single-family rental properties now require minimum coverage of £1 million, while multi-unit properties should consider umbrella policies providing additional protection above primary policy limits.

These increases reflect rising legal settlements and the growing complexity of tenant-related liability claims. Property managers handling multiple units particularly benefit from comprehensive umbrella coverage extending across their entire portfolio.

Frequently Asked Questions

Does landlord insurance cover tenants' contents?

No, landlord insurance does not cover tenants' personal belongings. Landlord policies protect the building structure and landlord-owned items like appliances or furnishings, but tenants must secure separate renters' insurance for their possessions. This distinction often creates confusion, but it's essential for both parties to understand their coverage responsibilities.

Is building insurance required by mortgage lenders?

Yes, mortgage lenders require building insurance as a condition of lending. Lenders mandate coverage that protects their financial interest in the property, typically requiring coverage amounts matching or exceeding the outstanding mortgage balance. For buy-to-let mortgages specifically, lenders often require landlord insurance rather than standard building insurance, recognizing the different risk profile of rental properties.

What's the difference between standard home insurance and landlord insurance?

Standard home insurance assumes owner-occupancy and covers personal liability scenarios typical of homeowners. Landlord insurance recognizes rental-specific risks including tenant-caused damage, liability from tenant guests, loss of rental income, and business-related claims. Additionally, landlord policies often exclude certain perils that homeowner's policies cover, such as tenant theft or intentional damage, requiring separate coverage considerations.

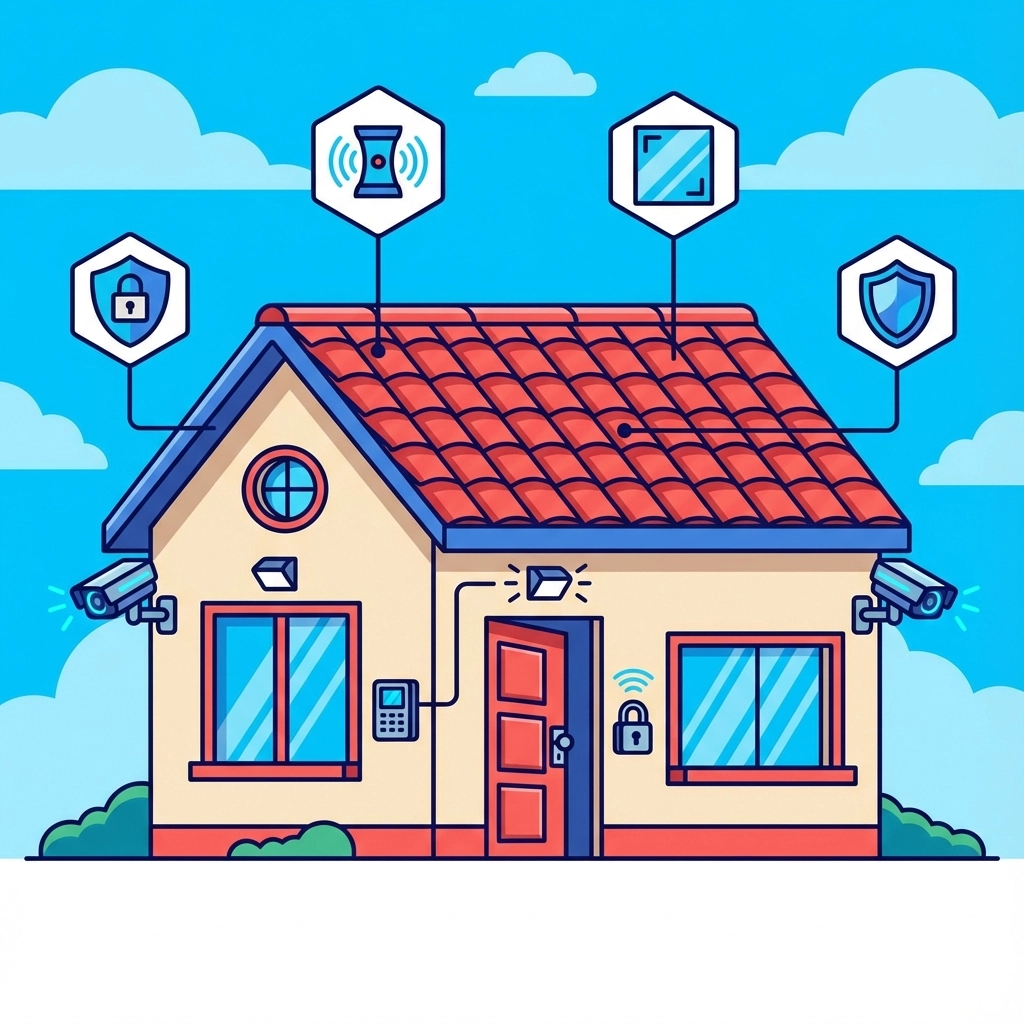

Property Hardening for Lower Premiums

Insurance providers in 2026 increasingly reward landlords investing in property resilience. Strategic upgrades can significantly reduce premiums while improving coverage availability:

Roof Improvements: Impact-resistant shingles or metal roofing meeting current wind standards demonstrate risk reduction commitment. Documentation from certified contractors often qualifies for immediate premium discounts.

Fire Prevention: Ember-resistant vents in wildfire-prone areas prevent airborne embers from entering attics, while electrical monitoring systems detect dangerous arcing before fires occur.

Flood Mitigation: Raised electrical systems and backflow valves in basement properties protect against water damage, particularly important as extreme weather events become more frequent.

Security Enhancements: Smart locks and security cameras provide both theft deterrence and liability documentation, helping defend against fraudulent injury claims.

Cost Considerations for 2026

Home insurance costs continue rising in 2026, though rates are stabilizing in many regions. Average homeowner's insurance costs approximately £2,400 annually for £300,000 dwelling coverage, with significant regional variations based on natural disaster risks and local construction costs.

Landlord insurance typically costs 25-50% more than equivalent homeowner's coverage due to increased risk exposure. However, several strategies can reduce premiums without compromising protection:

Shopping Strategy: Obtaining quotes from at least five different providers often reveals significant rate variations for identical coverage. Independent agents can streamline this process by accessing multiple carrier networks simultaneously.

Technology Discounts: Smart home devices including leak detectors, security systems, and electrical monitoring equipment qualify for discounts with many carriers. Documentation of installations and monitoring capabilities strengthens discount negotiations.

Portfolio Bundling: Landlords managing multiple properties often qualify for portfolio discounts when placing all coverage with single carriers. Some providers offer master policies covering entire rental property portfolios under unified management systems.

Top Insurance Providers for 2026

State Farm leads in comprehensive coverage and local support, particularly strong for single-family rental properties. Their extensive agent network provides face-to-face service that many landlords value for complex claims management.

Liberty Mutual excels in coverage customization, offering modular coverage riders including equipment breakdown, cyber liability, and specialized tenant-related protections. Their flexibility suits landlords with unique property types or risk profiles.

Allstate provides superior multi-property portfolio management with streamlined digital tools and consolidated billing. Their technology platform particularly benefits landlords managing numerous rental units across different locations.

Critical Planning Considerations

Risk assessment must precede coverage shopping. Location-specific risks including flood zones, storm patterns, and crime statistics directly impact coverage needs and premium costs. Property condition factors such as electrical system age, roof condition, and structural integrity influence both coverage availability and pricing.

Special liability considerations including swimming pools, trampolines, or older building features require specific coverage attention. These high-risk elements often necessitate additional liability coverage or separate policy riders.

Understanding policy exclusions proves crucial for avoiding coverage gaps. Standard policies typically exclude flood damage, requiring separate flood insurance policies in high-risk areas. Earthquake coverage, terrorism protection, and certain types of water damage often require specific policy riders or separate coverage.

For landlords seeking buy-to-let mortgages or portfolio expansion, proper insurance documentation streamlines the mortgage application process. Lenders increasingly scrutinize insurance coverage adequacy during underwriting, making comprehensive coverage essential for financing approval.

Facebook Summary:

Navigate 2026's complex insurance landscape with confidence. This comprehensive guide breaks down the crucial differences between homeowner's and landlord insurance, covering everything from mandatory lender requirements to cost-saving strategies. Get the protection your property investment deserves.